Provide Sustainable Electric Bikes For Everyone

Malesuada fames ac turpis egestas. Interdum velit laoreet id donec. Eu tincidunt tortor aliquam nulla facilisi cras.

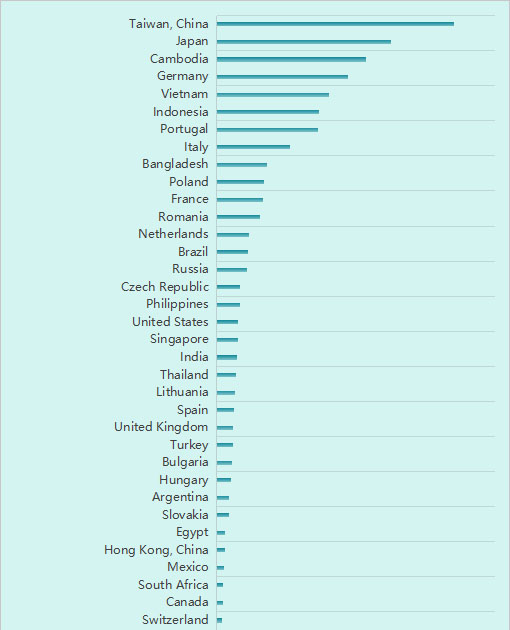

The data in the chart reflects China’s export volume of bicycle hubs—the core component of a bicycle’s wheel system that directly impacts transmission efficiency, ride quality, and durability. As a critical part of the bicycle supply chain, hubs demand high manufacturing precision and technical expertise.

Table of Contents

The export data reveals an extreme concentration effect across markets:

This structure directly mirrors the global division of labor in the bicycle industry: China is the undisputed manufacturing hub for bicycle hubs globally, with exports heavily reliant on a small number of core markets, while penetration in most global markets remains extremely low.

Taiwan is the “heart” of the global high-end bicycle industry (home to global top-tier brands like Giant, and a hub for R&D, OEM production, and brand operation). Meanwhile, mainland China is the global manufacturing base for bicycle components. The trade logic between the two is clear:

Deep Industrial Synergy: Taiwan’s bicycle OEMs/enterprises source hubs from mainland China for assembly, secondary processing, and supporting production—reflecting the deep integration of cross-strait bicycle supply chains.

Transshipment Hub Attribute: Taiwan’s local bicycle consumer market is small in scale. The hubs exported to Taiwan are mostly re-exported to global high-end markets (especially Europe and the US), making Taiwan China’s top destination for hub exports. This is a result of the global division of labor: “mainland China manufactures components, Taiwan leads branding and transshipment”.

The seven Tier 2 economies fall into three clusters, each with distinct trade drivers:

These three countries are the primary destinations for the global relocation of mid-to-low-end bicycle OEM capacity. In recent years, many Chinese and Taiwanese bicycle manufacturers have moved production to Southeast Asia. However, the region’s local component supply chain is highly underdeveloped and cannot meet demand for core parts like hubs, requiring bulk imports from China for local assembly before re-export to Europe and the US.

This trade flow is a direct outcome of the global division of labor: “China manufactures components, Southeast Asia assembles bikes”. It represents the core growth driver for China’s hub exports moving forward.

Europe is the global core consumer market for high-end bicycles (road bikes, mountain bikes, and E-bikes). Germany is Europe’s largest bicycle market, while Portugal and Italy are traditional European bicycle industry powers (home to numerous OEMs and brands).

European brands/OEMs have strong demand for mid-to-high-end hubs, and China—with the world’s most abundant hub production capacity and cost-effectiveness—serves as a key component supplier to the European bicycle industry, meeting local consumer demand.

Japan is a mature global bicycle consumer market and also home to Shimano, a global leader in top-tier bicycle components.

A portion of exports meets local demand for bicycle assembly and maintenance;

The other portion supports OEM production for Japanese component giants (e.g., mid-low-end Shimano hubs are manufactured in China and resold to Japan), forming a supply chain collaboration loop.

The Tier 3 cluster covers major global economies, categorized into three types:

Mature Western Consumer Markets: The US, France, the UK, Spain, the Netherlands, etc. These are core global bicycle consumption markets but rank lower than Tier 2. Key reasons: The US imports mostly complete bikes (reducing component demand); non-core European industrial countries focus on consumption with limited component supporting demand; and high-end markets are dominated by brands like Shimano and SRAM, with Chinese hubs primarily penetrating mid-to-low-end segments.

Emerging Markets: Bangladesh, India, Brazil, Russia, the Philippines, Thailand, etc. These markets have moderate local bicycle assembly capacity and steady maintenance demand, forming a stable “basic market” for China’s hub exports.

Hong Kong, China: A transshipment hub. Most hubs exported to Hong Kong are re-exported to other global markets (Southeast Asia, Europe, the US) rather than consumed locally, making it a key node in Greater China’s trade network.

Export volume is extremely low in most remaining countries for three core reasons:

Small Market Size: Most are small, low-income economies with limited bicycle consumption demand;

Missing Industrial Chain: Almost no local bicycle assembly capacity, eliminating bulk component procurement needs (only small retail/ maintenance demand);

High Trade & Logistics Costs: steep logistics costs and trade barriers in Africa, Latin America, and Central Asia deter Chinese exporters;

Competitor Substitution: Regional component manufacturers in India, Turkey, etc., capture market share, reducing China’s penetration.

The export data confirms the global bicycle industry’s division of labor will remain unchanged in the short term: China manufactures core components (hubs), Southeast Asia assembles bikes, and Europe/Japan lead branding, R&D, and consumption. China’s complete supply chain, extreme cost control, and abundant production capacity make it an irreplaceable component supplier to the global bicycle industry—a position set to solidify over the next 5–10 years.

Countries like Cambodia, Vietnam, and Indonesia are the primary destinations for global bicycle capacity relocation. As production capacity in these nations expands, demand for Chinese hubs will continue to grow. Risk Note: The local component industry in Southeast Asia (Vietnam, Thailand) is emerging and will displace mid-to-low-end Chinese hubs. Chinese companies must upgrade toward high-end, precision manufacturing to maintain technical barriers.

Chinese hubs currently have low penetration in European and American high-end markets, dominated by Shimano and SRAM. However, the global surge in E-bikes creates a game-changing opportunity: The European and US E-bike market is growing rapidly, with explosive demand for electric hubs and motorized hubs. Chinese companies hold technical and production advantages in electric components, enabling direct entry into high-end supply chains; For mid-to-high-end road/mountain bike markets, Chinese brands can penetrate via technical upgrades, quality improvements, and independent branding to displace imported brands.

The deep collaboration between Taiwan (high-end R&D/branding), Hong Kong (transshipment/finance), and mainland China (manufacturing) is the core of China’s global competitiveness in the bicycle industry. Future integration can deepen: Mainland China provides manufacturing capacity, Taiwan offers R&D and brand operation, and Hong Kong supports trade and financial services—forging a “China Super Cluster” for the global bicycle industry and enhancing global influence.

While small in scale now, African, Latin American, and Central Asian markets will see rapid growth in demand for commuter and E-bikes as economies develop. Chinese companies can capture future incremental demand by launching high-cost-performance products and establishing early market presence.

This export data is essentially a “barometer” of the global bicycle industry’s division of labor: China is the “world factory” for bicycle hubs, with exports heavily concentrated in Greater China, Southeast Asian capacity relocation hubs, and European/Japanese high-end markets, while penetration in most global markets remains minimal.

China’s core development path for the bicycle hub industry is clear: consolidate growth in Southeast Asian markets, break into European and American high-end markets, deepen Greater China supply chain integration, and layout emerging long-tail markets. Simultaneously, address trade barriers and Southeast Asian substitution to evolve from a “manufacturing power” to a “manufacturing powerhouse”.