Provide Sustainable Electric Bikes For Everyone

Malesuada fames ac turpis egestas. Interdum velit laoreet id donec. Eu tincidunt tortor aliquam nulla facilisi cras.

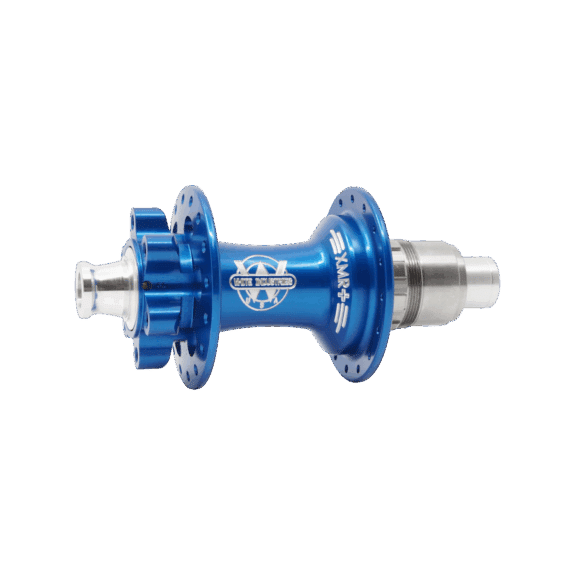

Product note: HS code 87149310 refers to bicycle hubs, freewheels, and chain-wheel/driving components – essential parts of a bicycle’s drivetrain.

Post-boom demand softened, but global shipping congestion forced some buyers to use expensive air freight, propping up order values.

COVID-related factory closures in Vietnam and Cambodia (2021) redirected orders back to China.

The 2022 energy crisis and Russia-Ukraine war drove up aluminium and steel prices, raising unit prices and offsetting some volume decline.

A multi-layered, irreversible shift:

Table of Contents

The golden era for Chinese exports of HS 87149310 to Japan peaked in 2020 and has entered an irreversible structural decline. Demographic shrinkage in Japan, deliberate supply-chain diversification away from China, technological substitution, and extreme currency volatility have reduced 2025 exports to just 12% of the 2020 level.

Unless Chinese manufacturers rapidly pivot to high-value products – such as e-bike hub motors, intelligent freewheels, or integrated drive systems – this product category will likely remain at very low levels for the foreseeable future.

If you need a strategic follow-up – e.g., product mix recommendations or alternative market options (Southeast Asia, Middle East) – please let me know.